ADHD Money Management: The Complete Guide to Financial Control for Neurodivergent Adults

It is the fifteenth of the month. You open your banking app and stare at the number on the screen. It makes no sense. You were paid two weeks ago, and your salary should cover everything comfortably—but the balance is already worryingly low. You try to retrace your spending. There was the impulsive online order at midnight on Tuesday. The coffee subscriptions you forgot to cancel. The parking ticket you paid because you forgot to renew your permit. The emergency grocery run where you bought seven items you did not need and forgot the two you came in for. The premium streaming service you signed up for during a hyperfocus session on documentaries that you have not opened since.

None of those purchases felt significant in the moment. That is exactly the problem.

For adults with Attention Deficit Hyperactivity Disorder (ADHD), financial instability is one of the most consistent and damaging consequences of neurodivergent executive dysfunction. Research published in the Journal of Attention Disorders consistently shows that adults with ADHD carry significantly higher debt burdens, save less for retirement, and experience more financial crises than their neurotypical peers—not because they lack intelligence or financial literacy, but because the executive skills required for sustainable **ADHD money management** are precisely the ones most compromised by the condition.

This guide provides a comprehensive, evidence-based framework for **money management for ADHD adults**. You will learn the neuroscience behind why **adhd finances** are structurally difficult to manage, discover how to build a low-friction **adhd budgeting** system that works with your brain rather than against it, and gain access to actionable templates, checklists, and expert-level strategies for achieving lasting financial stability. By implementing these specialized **ADHD money management** systems, you can stop the cycle of financial chaos and build a life where your bank account reflects your actual values and intentions.

Why the ADHD Brain Struggles with Money: The Neurological Foundation

Understanding the neurological basis of financial difficulty is the essential first step. **Money management** is not one skill; it is a complex bundle of executive functions performed consistently over time. Each of those executive functions is directly compromised by ADHD.

- Temporal Discounting and the Dopamine Deficit: The ADHD brain has a profoundly distorted relationship with time and future reward. The dopamine system—responsible for evaluating the value of future outcomes—is dysregulated in ADHD, causing the brain to dramatically undervalue rewards that occur in the future while overvaluing immediate gratification. This is why saving for retirement feels meaningless while buying something today feels urgent and rewarding. The technical term is “steep temporal discounting,” and it is a core neurological feature of ADHD, not a moral failing.

- Impulse Control Deficits: The prefrontal cortex provides the neural “braking system” that intercepts impulsive actions before they execute. In ADHD, this braking system is underactivated, meaning that the impulse to purchase something attractive—a sale, a gadget, a subscription—reaches behavioral execution before the rational evaluation of consequences has a chance to intervene. The purchase is made; the regret follows later.

- Working Memory and Financial Tracking: Sustaining a budget requires remembering multiple numbers and categories simultaneously over extended periods. Because ADHD significantly reduces working memory capacity, the brain cannot reliably hold account balances, upcoming bills, and spending categories in active memory. Information is simply not there when needed.

- Task Initiation and Administrative Avoidance: Bills, account reconciliation, tax preparation, subscription audits—these tasks are low-stimulation, high-effort, and contain no immediate reward. For the ADHD brain, they are precisely the type of activity that triggers the strongest avoidance response. The result is unopened bank statements, missed payment deadlines, and growing late fees.

- Hyperfocus Spending: The same hyperfocus mechanism that allows ADHD individuals to spend twelve hours mastering a new skill can hijack financial decision-making. A hyperfocus episode on a new hobby, a tech purchase, or a home project can result in hundreds or thousands of dollars in impulsive spending in a single session, completely bypassing rational budget awareness.

Symptoms of ADHD Financial Dysfunction

Recognizing the specific patterns of financial difficulty associated with ADHD is critical for choosing the right interventions. These symptoms of disrupted **adhd finances** are distinct from general financial mismanagement.

| Symptom | Neurological Driver | How It Appears in Daily Life |

|---|---|---|

| Chronic Impulse Purchasing | Dopamine-driven temporal discounting; weak prefrontal braking signals. | Frequent unplanned online orders, subscription sign-ups, and in-store purchases that felt urgent in the moment but are rarely used. |

| Late Fees and Missed Bills | Prospective memory failure; task initiation avoidance. | Consistent utility and credit card late fees despite having the money to pay on time. Bills are simply forgotten until a penalty notice arrives. |

| Subscription Accumulation | Novelty-seeking combined with poor tracking of recurring charges. | Paying monthly for 4–7 streaming, app, or service subscriptions, many of which are unused or forgotten. |

| Hyperfocus Spending Sprees | Sustained attention on a novel interest bypasses rational financial oversight. | Spending $600 on photography equipment during a weekend of hyperfocused interest that fades within two weeks. |

| Financial Avoidance | Administrative tasks trigger the ADHD avoidance response; shame compounds avoidance. | Unopened bank statements, unfiled tax returns, unread credit card statements, and actively avoiding checking account balances. |

| Income Instability | Career inconsistency caused by ADHD executive dysfunction. | Frequent job changes, performance-related terminations, or underemployment relative to intellectual capacity, creating irregular income patterns. |

Scientific Background: The ADHD Financial Research

The 30% Rule with ADHD and Financial Maturity

Dr. Russell Barkley’s **30% rule with ADHD** states that individuals with ADHD typically lag approximately 30% behind neurotypical peers in executive age and self-regulation capacity. For a 35-year-old professional with ADHD, their executive maturity in financial self-regulation is closer to that of a 24-year-old.

This developmental gap is critical for understanding **adhd budgeting** challenges. Society expects 35-year-olds to manage mortgages, retirement accounts, insurance policies, investment portfolios, and emergency funds—all financial products and decisions that require sustained executive capacity well beyond what that 24-year-old executive age can manage without external scaffolding. When ADHD adults are held to financial benchmarks designed for neurotypical developmental timelines, shame and failure are nearly inevitable without compensatory systems.

Research on ADHD and Financial Outcomes

Clinical research consistently documents the financial impact of ADHD across all age groups:

- Adults with ADHD are significantly more likely to have credit card debt and to carry balances month-to-month compared to neurotypical peers.

- Studies show that adults with ADHD have lower savings rates, smaller emergency funds, and less retirement preparation despite comparable or higher incomes.

- ADHD has been independently associated with higher rates of bankruptcy, financial hardship, and economic instability across US, UK, Canadian, and Australian populations.

These outcomes improve dramatically when ADHD is treated—through medication, coaching, and structural environmental design—confirming that the financial difficulties are a direct symptom of the neurological condition rather than a permanent character trait.

Real-World Financial Scenarios

Scenario A: Without a System (Claire’s Story)

Claire is a 33-year-old marketing manager in the UK with diagnosed ADHD. She earns a comfortable salary, is intellectually capable, and genuinely wants to save money—but every month ends with her confused about where her money went.

She has six active streaming subscriptions, three of which she has not used in months. She consistently pays late fees on her credit card because the statement arrives by post and gets buried under other mail. She experiences guilt every time she receives a bank notification and has stopped checking her balance to avoid the anxiety.

When a car repair bill arrives unexpectedly, she has no emergency fund and must put it on her credit card, increasing her debt. The debt generates shame, which deepens her avoidance of financial tasks, which generates more debt.

Without an ADHD-compatible financial system, each month’s financial fresh start is derailed by the accumulated debt, forgotten subscriptions, and missed payments of the month before.

Scenario B: Building Financial Scaffolds (Ravi’s Story)

Ravi, a 40-year-old software developer in Canada, had the same cycle for years. After his ADHD diagnosis at 37, he redesigned his entire **adhd finances** system around the principle of automation.

He spent one Saturday conducting a “subscription audit,” cancelling every recurring charge he could not justify. He set up auto-pay on every monthly bill—utilities, insurance, credit card minimums, streaming services—eliminating the need for prospective memory entirely.

He opened a separate savings account at a different bank with automatic weekly transfers of $75. Because the account was at a different bank, it was harder to see and access impulsively.

He also began a practice he called “the 48-hour rule”: any non-essential purchase over $50 was added to a wishlist. If he still wanted it 48 hours later, he could buy it. This single strategy eliminated approximately 60% of his impulsive purchases.

Within six months, his late fees had dropped to zero, he had built a small emergency fund for the first time, and his financial anxiety had decreased significantly.

Scenario C: Managing Money in Partnerships

Sofia and Marcus have been together for four years. Marcus has ADHD and Sofia does not. Their financial disagreements were a recurring source of conflict—not because Marcus was careless about money, but because their approaches to financial tracking were fundamentally incompatible.

Sofia managed finances using detailed spreadsheets and monthly budget reviews. Marcus found these sessions overwhelming and avoided them, which Sofia experienced as disinterest. Marcus’s impulsive purchases disrupted Sofia’s carefully planned budgets, which she experienced as disrespect.

After reading about **money management for ADHD adults**, they redesigned their system. They opened a joint account for shared household expenses, funded automatically each month from both salaries. Personal discretionary accounts allowed Marcus freedom to spend without disrupting shared finances.

Marcus used the ADHD Daily Planner to set a weekly “money check-in” appointment—just 10 minutes of reviewing his personal account balance and upcoming expenses. Sofia continued her detailed spreadsheets for shared finances. The hybrid system respected both their neurological styles and eliminated the source of most of their financial conflict.

The ADHD Money Management Framework: A Step-by-Step System

The core principle of ADHD-compatible **adhd budgeting** is this: never trust your future self to remember, decide, or initiate a financial task in the moment it is due. Automate everything that can be automated, externalize everything that cannot, and protect your executive energy for choices that genuinely require it.

Phase 1: The Financial Audit (One-Time Foundation)

This is the most uncomfortable step but the most essential. Set aside two uninterrupted hours with your bank statements and a notepad.

- The Subscription Purge: Review every recurring charge on your bank and credit card statements for the past three months. List every subscription. Cancel any that you have not actively used in the past 30 days. Use an app such as Rocket Money (US), Emma (UK), or PocketGuard (Canada/Australia) to identify hidden recurring charges automatically.

- The Bill Inventory: List every bill you pay monthly, quarterly, and annually. Record the amount, due date, and payment method for each. This becomes your master reference document.

- The Debt Map: Write down every debt: credit cards, student loans, car payments, and any informal debts. Record the balance, interest rate, and minimum payment for each. This is often anxiety-inducing—do it anyway. You cannot manage what you cannot see.

Phase 2: The Automation Architecture

After the audit, your primary goal is to remove as many recurring financial decisions as possible from your active attention.

- Auto-Pay Every Fixed Bill: Set up automatic payments for every bill with a fixed amount—utilities, insurance, phone, internet, subscriptions. For variable bills like credit cards, set auto-pay for at least the minimum payment to prevent late fees while you manage the remaining balance manually.

- The Pay-Yourself-First Savings Transfer: Set up an automatic transfer to a savings account that triggers on the day after your salary arrives. Start with any amount—even $20 per week. The act of automating savings is more important than the initial amount.

- Separate Savings at a Separate Bank: Open a savings account at a different institution from your primary checking account. The friction of transferring money back reduces impulsive withdrawals significantly.

- Emergency Fund Naming: Naming your savings account “Emergency Fund Only” or “Car Repair” in your banking app activates a subtle psychological barrier to spending it on non-emergencies—a simple but consistently effective strategy.

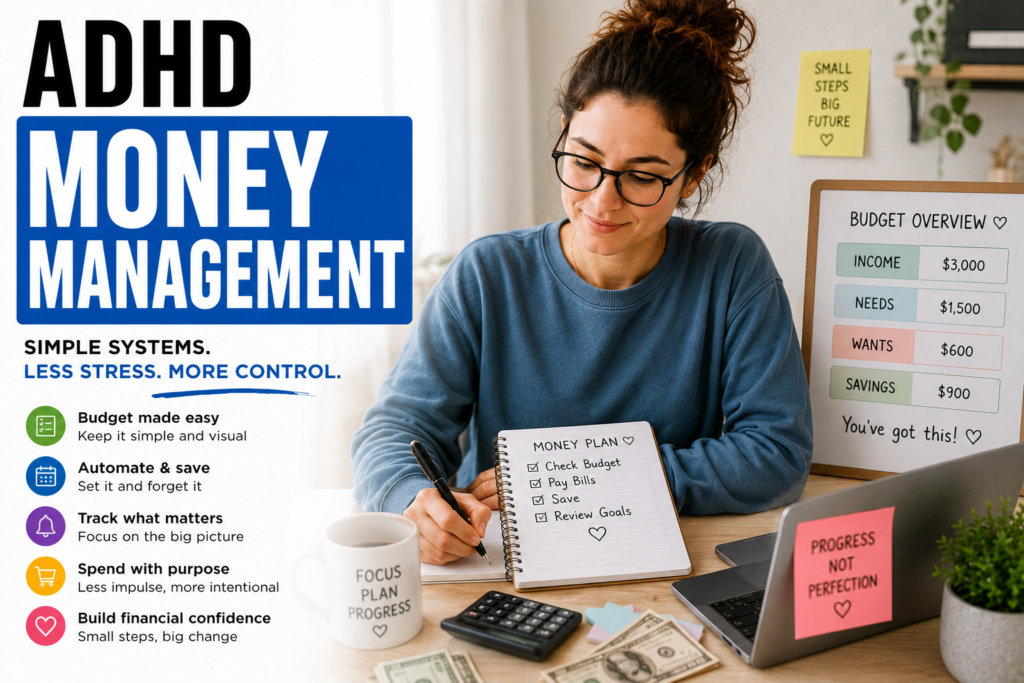

Phase 3: The ADHD-Compatible Budget System

Traditional budgets fail adults with ADHD because they require continuous, detailed tracking—the cognitive equivalent of asking someone who cannot see to navigate by sight. The ADHD budget system instead uses broad, automated categories.

- The Three-Account System:

- Bills Account: A dedicated account into which a fixed amount is deposited automatically each payday to cover all recurring bills. This account is never used for discretionary spending.

- Spending Account: Your day-to-day account. Every dollar remaining after bills and savings are funded is here. When this account is empty, spending stops for the month. No tracking categories, no detailed receipts—just a hard boundary.

- Savings Account: Auto-funded each payday. Separated at a different bank. Touched only for genuine emergencies or planned goals.

- The Weekly Money Date: Schedule a recurring 15-minute “money check-in” appointment in your calendar or ADHD Daily Planner. Use this time only to review your spending account balance and upcoming expenses for the week. Do not attempt to reconcile your full budget or analyze spending categories—that level of detail is unsustainable for most ADHD brains.

- The 48-Hour Rule: Any non-essential purchase over a personal threshold (e.g., $30–$100) goes onto a written wishlist for 48 hours before purchase. Many purchases will feel unnecessary after the dopamine spike of discovery has passed.

Phase 4: Debt Reduction Strategy

Managing debt with ADHD requires a system that is simple, visible, and provides regular dopamine reward.

- The Snowball Method: List all debts from smallest to largest balance, regardless of interest rate. Pay the minimum on all except the smallest. Direct every available extra dollar at the smallest debt until it is eliminated, then roll that payment to the next smallest. The frequent “wins” of fully paid debts generate dopamine that keeps you motivated through the process.

- Visualize Your Progress: Create a simple visual debt tracker on paper or a whiteboard. Color in a segment each time you make a payment. The visual evidence of progress is a powerful ADHD motivator.

- Break Tasks with the ADHD Task Breakdown Tool: Financial tasks like calling a creditor to negotiate a rate or organizing documents for tax preparation feel overwhelming as single tasks. Break each one into individual, five-minute micro-steps to overcome initiation barriers.

Printable ADHD Financial Templates

Template 1: The ADHD Monthly Financial Dashboard

Automated Deductions (Set and Forget):

• Bills Account Transfer: $_________ (Auto on payday)

• Savings Transfer: $_________ (Auto day after payday)

Remaining Spending Account Balance: $_____________ (This is your monthly limit)

This Month’s Wishlist (48-Hour Rule):

1. _________________________________ Added: _______ Buy/Skip: _______

2. _________________________________ Added: _______ Buy/Skip: _______

3. _________________________________ Added: _______ Buy/Skip: _______

Debt Tracker (Snowball Method):

• Smallest Debt: _________________ Balance: $_______ Extra payment this month: $_______

• Next Debt: _________________ Balance: $_______ (minimum payment only)

Weekly Money Date Completed: [ ] Week 1 [ ] Week 2 [ ] Week 3 [ ] Week 4

Template 2: Subscription Audit Sheet

| Subscription Name | Monthly Cost | Used in Last 30 Days? | Action |

|---|---|---|---|

| Netflix | $15.49 | [ ] Yes [ ] No | [ ] Keep [ ] Cancel [ ] Downgrade |

| Gym Membership | $45.00 | [ ] Yes [ ] No | [ ] Keep [ ] Cancel [ ] Pause |

| Cloud Storage | $2.99 | [ ] Yes [ ] No | [ ] Keep [ ] Cancel [ ] Downgrade |

| News App | $12.99 | [ ] Yes [ ] No | [ ] Keep [ ] Cancel [ ] Downgrade |

| ________________________ | $_______ | [ ] Yes [ ] No | [ ] Keep [ ] Cancel [ ] Other |

| Total Monthly Subscriptions: | $_______ | Annual Cost: $____________ | |

Expert Recommendations and Clinical Pathways

If financial difficulties are significantly impacting your wellbeing, relationships, or career stability, professional support can provide targeted guidance:

- ADHD-Informed Financial Therapists: Financial therapy combines financial planning with therapeutic support around the emotional and psychological components of money management. Look for therapists who are members of the Financial Therapy Association (FTA) with experience in neurodivergent clients.

- Credit Counseling Services: Non-profit credit counseling agencies (such as NFCC in the US or StepChange in the UK) provide free or low-cost debt management plans and budgeting support without judgment.

- ADHD Coaching: An ADHD coach can help you implement and troubleshoot your financial automation system, create accountability for weekly money check-ins, and build the routine structures that sustain long-term financial stability.

Regional Financial and ADHD Support Resources

- United States: CHADD provides directories for ADHD specialists; NFCC offers free non-profit credit counseling.

- United Kingdom: The ADHD Foundation offers coaching referrals; StepChange provides free debt management support.

- Canada: CADDAC provides adult ADHD resources; Credit Counselling Canada offers provincial support.

- Australia: ADHD Australia connects individuals with specialists; the National Debt Helpline (1800 007 007) provides free financial counseling.

Frequently Asked Questions

Why is money management so hard with ADHD?

Money management requires sustained working memory, prospective memory, impulse inhibition, and the consistent initiation of low-stimulation administrative tasks—precisely the executive skills most compromised by ADHD. Additionally, ADHD’s dopamine dysregulation causes the brain to dramatically undervalue future financial rewards (like savings) in favor of immediate purchasing gratification.

What is the best budgeting system for ADHD?

The most effective **adhd budgeting** system is one that requires the least ongoing active decision-making. The Three-Account System (Bills, Spending, Savings) combined with full automation of recurring payments eliminates the need for continuous tracking. Supplement with a weekly 15-minute money check-in rather than detailed daily logging.

How do I stop impulse spending with ADHD?

The most effective strategy is the 48-Hour Rule: add any non-essential purchase above your personal threshold to a written wishlist and wait 48 hours before buying. Additional strategies include disabling one-click purchasing on Amazon, removing saved payment details from shopping websites, and using a cash-only system for discretionary spending categories.

How do I save money with ADHD?

Automate saving so it requires no active decision. Set up a direct debit or automatic transfer from your salary account to a savings account on the day after your payday. Place the savings account at a different bank to create friction against impulsive withdrawals. Start with any amount—consistency matters more than the sum.

Does ADHD medication help with financial management?

Yes. Stimulant and non-stimulant ADHD medications improve prefrontal cortex function, which strengthens impulse control, working memory, and the capacity to delay gratification—all of which directly improve financial decision-making. However, medication alone is insufficient; structural systems like automation and the three-account framework are essential complements.

Conclusion: Financial Stability Is a System, Not a Character Trait

Financial instability in adults with ADHD is not a reflection of intelligence, work ethic, or values. It is the entirely predictable consequence of asking a neurodivergent brain to manage complex, long-horizon financial decisions using only willpower and memory—two resources that ADHD depletes daily.

The solution is not to become a different type of person. The solution is to build a financial infrastructure so robust that it functions reliably even when your executive system is at its most depleted.

Start today with one step. Set up auto-pay on your next upcoming bill. Run your subscription audit. Open a separate savings account and transfer $25. Every single automated system you put in place is one fewer decision your brain must make—and one step closer to a financial life that reflects who you truly are.